The Great Coffee Contradiction: Supply Fears Meet Surplus Forecasts

Coffee prices are a puzzle today. Global mixed, local down, but a deeper dive reveals supply shortages battling surprising surplus predictions. Decode the future.

Today's Brew: A Snapshot of Market Movements

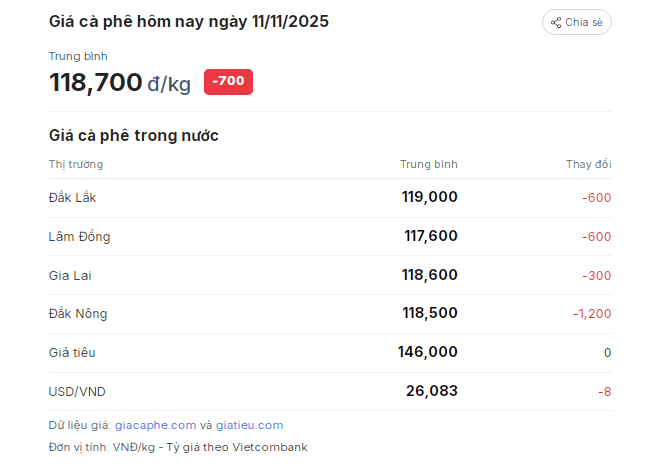

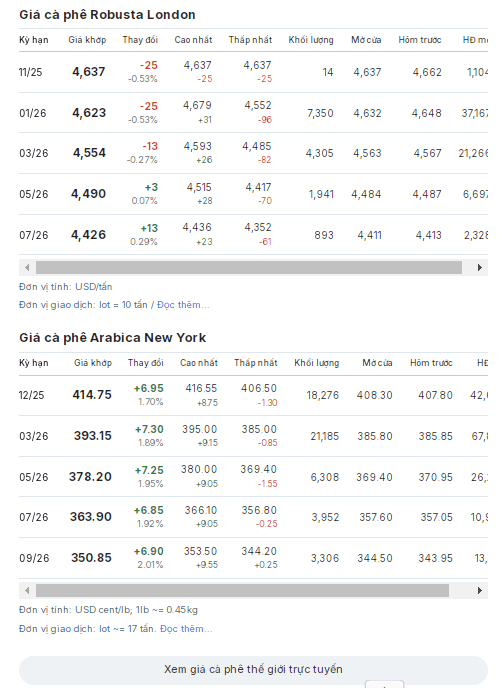

The global coffee market is a fascinating blend of contrasting trends, and today's movements offer a prime example. While futures on the New York exchange saw a notable ascent, contracts in London experienced a slight dip. Specifically, Arabica for December 2025 delivery climbed 1.7%, adding 6.95 US cents per pound to reach 414.75 US cents, with March 2026 contracts also gaining. Meanwhile, Robusta futures for November 2025 delivery on the London market edged down by 0.53%, shedding 25 USD per ton to settle at 4,637 USD. January 2026 contracts followed suit, dropping to 4,623 USD per ton. This mixed global picture, where one major bean gains ground while the other retreats, sets an intriguing backdrop for local markets. In , often considered the heart of its coffee production, farmers observed a uniform decrease in prices today, ranging from 300 to 1,200 Vietnamese Dong per kilogram. Prices across key provinces like (119,000 VND/kg), (118,600 VND/kg), , and (118,500 VND/kg) reflect this downward shift, oscillating between 117,600 and 119,000 VND/kg. The immediate takeaway? A day of divergence on the international stage, met by a unified, albeit slight, decline in Vietnam.

Global Futures on the Boil: Arabica's Ascent vs. Robusta's Dip

Delving deeper into the futures market reveals the underlying dynamics driving these divergent paths. The modest retreat in Robusta prices on the London exchange, as seen in the 0.53% drop for both November 2025 and January 2026 contracts, suggests a slight easing in immediate supply pressure or a reaction to broader market sentiment. Conversely, Arabica's robust performance in New York, with December 2025 contracts surging 1.7% and March 2026 contracts up 1.89%, points to stronger bullish conviction for the milder bean. This upward momentum for Arabica is partly attributed to the strengthening against the , which can make dollar-denominated coffee exports from less attractive, thus tightening perceived supply. Adding to Arabica's supply concerns, , a leading producer of washed Arabica, reported a 10% year-on-year drop in coffee output for October. These immediate supply-side factors for Arabica stand in stark contrast to broader forecasts, with the 's mid-2025 report projecting a global coffee surplus of nearly 10 million bags for the 2025/26 crop year. This early glimpse into a potential future oversupply creates a fascinating tension against the current market's immediate reactions.

Vietnam's Harvest Hopes and Local Price Realities

While global futures grapple with their own internal contradictions, are navigating a unique landscape of harvest optimism tempered by daily price fluctuations. Despite the day's slight dip of 300 to 1,200 VND/kg across the , pushing prices to between 117,600 and 119,000 VND/kg, the mood among farmers remains generally buoyant. Many are currently engrossed in the new harvest season, buoyed by expectations of a good yield this year and the prevailing high prices compared to previous seasons. Analysts highlight that is well-positioned to capitalize on global production shortfalls, particularly those in and , which have been hit hard by extreme weather events. This means that even with slight daily price adjustments, the overarching narrative for Vietnamese coffee remains positive, supported by global supply tightness and a weaker , which collectively enhance the commodity's appeal to investors. The local market, therefore, acts as a critical barometer, reflecting both immediate selling pressures and the long-term strategic advantage holds in a supply-constrained world.

The Looming Supply Debate: Scarcity Narratives Clash with Surplus Projections

The coffee market finds itself at a peculiar crossroads, where immediate scarcity narratives collide with significant long-term surplus projections. On one hand, compelling evidence points to current supply tightness: the reported a 0.3% decrease in global coffee exports for the 2024/25 crop year (October to September) compared to the previous season, totaling 138.658 million bags. Market analysts further underscore these concerns, attributing global price support to ongoing supply shortages from the new crop, alongside the disruptive impact of extreme weather in key producing nations like and . The 10% decline in Arabica production in October only adds to this picture of a constrained market. Yet, juxtaposed against these immediate worries is the 's mid-2025 report, which paints a dramatically different future. For the 2025/26 crop year, the USDA forecasts global production at 178.7 million bags against a consumption of 169.36 million bags, implying a substantial surplus of nearly 10 million bags. Other forecasts, while varying in magnitude, also anticipate a surplus of 4 to 5 million bags. This stark divergence creates considerable uncertainty, as major , for instance, continue to voice concerns about potential supply shortages extending into the 2025-2026 season, directly challenging the USDA's optimistic outlook.

Beyond the Bean: Navigating Coffee's Unpredictable Road Ahead

The intricate dance between immediate supply fears and long-term surplus forecasts makes navigating the coffee market an exercise in constant vigilance. The current strength in coffee prices, particularly for , is undeniably propped up by reports of tightening global supplies, adverse weather conditions in major growing regions like and , and a favorable weaker making coffee more attractive to international buyers. recent 10% dip in Arabica output further solidifies the 'scarcity now' narrative. However, the projection of a significant global surplus for the upcoming 2025/26 crop year looms large, creating a fundamental tension that market participants must reconcile. Will the anticipated bumper crops materialize fully, or will unexpected climate events or geopolitical shifts continue to disrupt supply chains? The concerns voiced by some about persistent shortages for 2025-2026 highlight that not everyone is convinced by the surplus predictions. This perplexing contradiction signals an unpredictable road ahead for coffee, where short-term volatility could give way to longer-term price adjustments, impacting everyone from the smallholder farmer in to the multinational roaster. Staying informed on these converging and diverging trends will be key to understanding coffee's future stability.

Related Articles

Turbulence in the Bean Market: Unmasking the Power Plays Behind Coffee Prices

Turbulence in the Bean Market: Unmasking the Power Plays Behind Coffee Prices

Coffee's August Surge: Decoding the Market's Unpredictable Brew

Coffee's August Surge: Decoding the Market's Unpredictable Brew

Brewing a New Reality: The Unseen Forces Behind Coffee's Historic Climb

Brewing a New Reality: The Unseen Forces Behind Coffee's Historic Climb

The Golden Bean Rush: Asia's Ascent and the Rewriting of Global Coffee Prices